Indians can buy 100% freehold Dubai property with no residency visa required. RBI LRS allows USD 250,000 annual remittance (₹2.1 Cr) with 20% TCS on amounts exceeding ₹10 lakhs. UAE has zero income/capital gains tax. India-UAE DTAA prevents double taxation. NRIs can repatriate USD 1M annually to India.

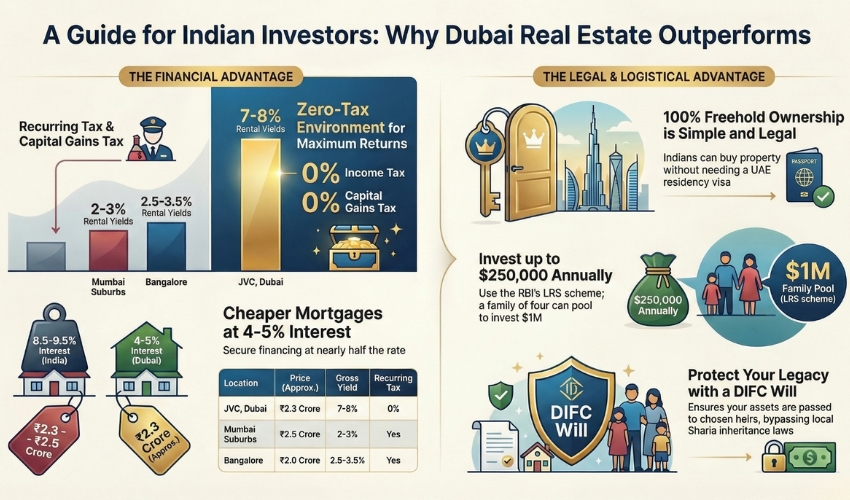

For Indian expats and NRIs, Dubai represents more than just tax-free salaries and modern infrastructure—it’s the ideal second home and wealth preservation strategy. With Mumbai apartments costing ₹2-3 crores for 600 sq ft and delivering 2-3% yields, Dubai’s AED 1M (₹2.3 Cr) properties offer 900 sq ft with 7-8% returns and zero taxation.

Here’s your complete roadmap to navigating RBI regulations, tax treaties, and securing your Dubai property investment.

Can Indians Legally Buy Property in Dubai?

Yes, with 100% freehold ownership rights in designated areas. No UAE residency visa is required to purchase, making Dubai more accessible than many Western markets.

Freehold Zones for Indians:

▫️ Jumeirah Village Circle (JVC) – Highest Indian expat concentration

▫️ Dubai Marina – Premium waterfront living

▫️ Business Bay – DIFC proximity for finance professionals

▫️ Downtown Dubai – Burj Khalifa district prestige

▫️ Dubai South – Airport connectivity

Bonus Visa Benefits:

▫️ AED 750,000+ investment = 2-Year Investor Visa eligibility

▫️ AED 2 Million+ investment = 10-Year Golden Visa (extends to spouse, children, parents)

▫️ Property ownership ≠ automatic visa (separate application required)

Key Advantage Over Other Markets: Unlike the UK (stamp duty 2-15%) or Singapore (additional buyer stamp duty 60% for foreigners), Dubai charges only 4% DLD registration fee with no recurring property taxes.

How Much Money Can Indians Send to Buy Dubai Property?

Reserve Bank of India’s Liberalised Remittance Scheme (LRS) governs overseas property investments.

LRS Limits & TCS Rules:

Annual Remittance Cap:

▫️ USD 250,000 per person (approximately ₹2.1 Crores at current rates)

▫️ Family pooling allowed: 4-member family = USD 1 Million collective limit

▫️ Resets every financial year (April 1)

Tax Collected at Source (TCS):

▫️ 20% TCS on amounts exceeding ₹10 Lakhs for property investment

▫️ Example: Remitting ₹50 Lakhs = ₹10 Lakhs TCS deducted upfront

▫️ Adjustable credit: TCS adjusts against final income tax liability (not a permanent cost)

Strategic Timing: For properties exceeding USD 250K, stagger payments across financial years or pool family limits to stay within LRS thresholds.

Required Documentation:

▫️ Form A2 (RBI foreign remittance declaration)

▫️ PAN card

▫️ Property purchase agreement

▫️ CA certification for amounts exceeding limits

Can Indians Get Mortgages for Dubai Property?

Yes, both UAE residents and NRIs qualify for Dubai property financing.

Mortgage Terms for Indians:

UAE Resident Indians:

▫️ Loan-to-Value: Up to 80% (20% down payment)

▫️ Salary requirement: Minimum AED 10,000-15,000 monthly

▫️ Interest rates: 4-5% (versus India’s 8.5-9.5%)

Non-Resident Indians (NRIs from India):

▫️ Loan-to-Value: 50-60% (40-50% down payment required)

▫️ Interest rates: 4.5-5.5%

▫️ Preferred lenders: Bank of Baroda UAE, ICICI Bank UAE, Emirates NBD

Comparative Advantage:

| Aspect | Dubai Mortgage | India Home Loan |

| Interest Rate | 4-5% | 8.5-9.5% |

| Processing Time | 2-3 weeks | 4-6 weeks |

| Property Tax | Zero | 0.2-0.5% annually |

| Rental Yield | 7-8% | 2-3% |

Monthly Payment Example: AED 1M property, 80% mortgage (AED 800K), 4.5% interest, 25 years = AED 4,450/month (versus AED 4,500-5,000 rental income = cash-flow positive from Day 1).

What Are the Tax Benefits of Dubai Property for Indians?

Dubai’s zero-tax environment combined with India-UAE DTAA creates powerful advantages.

Dubai Tax Structure:

▫️ Zero income tax on rental earnings

▫️ Zero capital gains tax on property sale profits

▫️ Zero inheritance tax

▫️ Zero wealth tax

India Tax Implications (Resident Indians):

Rental Income:

▫️ If UAE tax resident: Generally no Indian tax (claim DTAA benefits)

▫️ If Indian resident: Must declare global income in ITR, but DTAA prevents double taxation

▫️ Claim foreign tax credit or exemption under DTAA Article 6

Capital Gains on Sale:

▫️ Tax-free in Dubai regardless of holding period

▫️ Indian residents: May face LTCG (20% after indexation) or STCG (per income slab)

▫️ DTAA provides relief mechanisms to avoid paying twice

Wealth Preservation Advantage: Dubai property appreciating 8-10% annually + 7-8% rental yield + zero taxation = effective 15-18% annual returns versus India’s 5-7% post-tax returns.

Can Indians Bring Dubai Property Profits Back to India?

Yes, through structured repatriation channels.

Repatriation Process for NRIs:

Annual Limit:

▫️ USD 1 Million per financial year from NRO account (Non-Resident Ordinary)

▫️ Requires CA certification and RBI compliance

Required Forms:

▫️ Form 15CB: CA certificate for foreign remittance

▫️ Form 15CA: Self-declaration to Income Tax Department

▫️ Property sale documentation

▫️ Proof of original investment source

Timeline: 7-14 days for compliant documentation and bank processing.

Tax Optimization: Time property sales strategically across financial years to maximize repatriation limits and minimize tax impact using DTAA provisions.

Why Do Indian Expats Need a DIFC Will?

Critical for non-Muslim asset protection. UAE’s default Sharia inheritance laws may not align with Indian succession preferences.

DIFC Wills Solution:

Without DIFC Will (Sharia Law):

▫️ Male heirs receive double female heirs’ share

▫️ Spouse may receive only 1/8th of estate

▫️ Complex distribution formulas

▫️ Lengthy probate (6-18 months)

With DIFC Will (Your Choice):

✅ Specify exact beneficiaries (spouse, children, parents)

✅ Bypass Sharia law entirely for non-Muslims

✅ Faster estate settlement (3-6 months)

✅ Covers all UAE assets (property, bank accounts, investments)

Registration Process:

▫️ Visit DIFC Wills Service Centre

▫️ Bring Emirates ID, passport, property title deeds

▫️ Cost: AED 10,000-15,000 (one-time)

▫️ Update when buying/selling property

Peace of Mind: Ensures your JVC apartment transfers to your spouse/children exactly as intended, not per Sharia formula.

Where Should Indians Invest in Dubai?

While historical Indian communities thrived in Bur Dubai and Karama (older freehold-limited areas), modern investors prioritize high-yield freehold zones.

Top Choice: Jumeirah Village Circle (JVC)

Why Indians Love JVC:

Community Familiarity:

▫️ Largest Indian expat concentration in Dubai

▫️ JSS International School within community (CBSE curriculum)

▫️ Indian restaurants, grocery stores (Nesto, Lulu)

▫️ Hindi-speaking neighbors and support networks

Investment Fundamentals:

▫️ Pricing: AED 900K-1.15M for 1-bedroom (₹1.95-2.5 Cr)

▫️ Rental yields: 7-8% gross (versus Mumbai’s 2-3%)

▫️ Appreciation: 15-23% in recent years

▫️ Liquidity: Highest transaction volume = easy resale

Comparative Analysis (1-Bedroom Apartment):

| Location | Price | Yield | Taxes | Net Return |

| JVC Dubai | ₹2.3 Cr | 7-8% | 0% | 7-8% + appreciation |

| Mumbai Suburbs | ₹2.5 Cr | 2-3% | Property tax | ~1.5-2% net |

| Bangalore | ₹2 Cr | 2.5-3.5% | Property tax | ~2-2.5% net |

Infrastructure Catalyst: Metro Blue Line (operational 2029) station proximity to JVC District 11 projects 15-25% additional appreciation by completion.

Sereno Residences: Built for Indian Investors

Svarn Development understands Indian investment priorities: Vaastu principles, spacious layouts, transparent pricing, and RBI-compliant payment structures.

Why Sereno Residences Works for Indians:

▫️ Flexible Payment Plans: 40% post-handover aligns with LRS annual limits

▫️ District 11 Location: Best commute access (20 mins to Business Bay)

▫️ Modern Layouts: 900+ sq ft 1-beds (versus cramped 600 sq ft in older buildings)

▫️ Indian Community: JSS School 10-min drive, Circle Mall with Indian groceries walkable

▫️ Direct Developer Purchase: Zero agent commission saves AED 20,000-25,000

Investment Case for Mumbai/Delhi Residents:

▫️ Similar price point (₹2.3 Cr) buys 50% more space in Dubai

▫️ Triple the rental yield (7-8% vs 2-3%)

▫️ Zero taxation versus India’s property tax + income tax on rent

▫️ Currency diversification hedge against rupee depreciation

Your Dubai Property Roadmap

Indians have invested over USD 4 billion in Dubai real estate—it’s proven, tested, and legally sound. With RBI’s LRS providing clear frameworks and India-UAE DTAA eliminating double taxation fears, the process is straightforward.

Key Takeaways:

1. Legal: 100% freehold ownership, no visa required to buy

2. Financial: USD 250K annual LRS limit, 20% TCS (adjustable)

3. Taxation: Zero in Dubai, DTAA protects in India

4. Mortgages: 50-80% LTV at 4-5% interest

5. Legacy: DIFC Wills ensure Indian succession preferences

Ready to diversify beyond India? Sereno Residences offers turnkey solutions for Indian investors—from LRS-friendly payment plans to post-sale rental management.

Your Dubai journey starts with understanding the rules. It succeeds with choosing the right partner.

FAQs

Q. Can Indians buy property in Dubai without living there?

Indians can buy Dubai property without UAE residency. No visa required for purchase in 100% freehold zones (JVC, Marina, Business Bay, Downtown). Process: transfer funds via RBI LRS (USD 250K limit), select property, sign SPA, receive title deed. Properties worth AED 750K+ make buyers eligible for 2-Year Investor Visa (separate application). NRIs and resident Indians have identical purchase rights.

Q. How much money can I send from India to buy Dubai property?

USD 250,000 per person annually under RBI’s Liberalised Remittance Scheme (LRS). Family pooling allowed: 4-member family = USD 1M collective. 20% TCS (Tax Collected at Source) applies on remittances exceeding ₹10 lakhs for property investment—adjustable against income tax liability. For properties above USD 250K, stagger payments across financial years or use family pooling to stay within limits.

Q. Do I pay tax on Dubai property rental income in India?

Depends on tax residency. If UAE tax resident: generally no Indian tax (claim DTAA exemption). Indian resident: must declare global income in ITR, but India-UAE DTAA prevents double taxation—claim foreign tax credit or exemption under DTAA Article 6. Dubai charges zero income tax on rentals. Consult CA to structure properly and leverage DTAA benefits for tax optimization.

Q. Can NRIs get home loans for Dubai property?

Yes, NRIs can get Dubai mortgages from UAE banks. Terms: (1) 50-60% LTV (40-50% down payment), (2) 4.5-5.5% interest rates (lower than India’s 8.5-9.5%), (3) No Indian income consideration (Dubai income or global assets evaluated). Preferred lenders: Bank of Baroda UAE, ICICI Bank UAE, Emirates NBD. UAE resident Indians get better terms: 80% LTV, 4-5% rates.

Q. Is Dubai property better investment than Mumbai or Bangalore?

Dubai offers superior yields and zero taxation: JVC 1-bedroom costs similar to Mumbai suburbs (₹2.3 Cr) but delivers 7-8% yields (vs Mumbai’s 2-3%), zero property tax (vs India’s 0.2-0.5% annually), zero income tax on rent, and zero capital gains tax on sale. Infrastructure catalysts (Metro Blue Line) drive 15-25% appreciation. India advantages: local knowledge, easier management, rupee-denominated. Diversification across both markets is ideal.

Q. What is TCS on Dubai property purchase from India?

Tax Collected at Source (TCS) is 20% on LRS remittances exceeding ₹10 lakhs for property investment. Example: Remitting ₹50 lakhs = ₹10 lakhs TCS deducted at source. Not a permanent cost—TCS adjusts against final income tax liability when filing ITR. Claim refund if TCS exceeds actual tax due. Calculate effective cost: if in 30% tax bracket, ₹10L TCS for ₹50L remittance = ₹8.5L eventual refund.

Q. Can I bring Dubai property sale money back to India?

Yes, NRIs can repatriate USD 1 million annually from NRO account (Non-Resident Ordinary) to India. Process: (1) Sell Dubai property, (2) Deposit proceeds in NRO account, (3) Obtain CA certificate (Form 15CB), (4) Submit self-declaration (Form 15CA), (5) Bank processes transfer (7-14 days). Provide property sale docs and proof of original investment source. Resets each financial year (April 1).

Q. Do I need DIFC Will if I buy Dubai property as an Indian?

Highly recommended for non-Muslim Indians. Without DIFC Will, UAE’s default Sharia inheritance laws apply: male heirs receive double female heirs’ shares, spouses may get only 1/8th estate, complex distribution formulas. DIFC Wills allow non-Muslims to specify exact beneficiaries (spouse, children, parents), bypass Sharia, and ensure Indian succession preferences. Cost: AED 10,000-15,000 one-time. Covers all UAE assets including property.

Q. Which Dubai area is best for Indian expats investment?

Jumeirah Village Circle (JVC) offers best value for Indian investors:

(1) Largest Indian expat community (familiar culture, Hindi speakers),

(2) JSS International School within community (CBSE curriculum),

(3) 7-8% rental yields (highest in affordable segment),

(4) AED 900K-1.15M 1-beds (₹1.95-2.5 Cr),

(5) Indian grocery stores, restaurants,

(6) Metro Blue Line proximity (15-25% appreciation catalyst by 2029).

District 11 offers best infrastructure access.

Q. How does India-UAE DTAA work for property investors?

Double Taxation Avoidance Agreement (DTAA) ensures Indians don’t pay tax twice on Dubai property income. Rental income: Dubai charges 0%, India taxes global income for residents—claim foreign tax credit or exemption under DTAA Article 6 when filing ITR. Capital gains: Dubai charges 0% on sale, India may tax LTCG/STCG for residents—DTAA provides relief. Consult CA to structure and claim benefits properly.

Q. Can I use Indian income to get a Dubai property mortgage?

For NRIs: Dubai banks typically don’t consider Indian salary income—evaluate UAE employment income or global assets. Exception: Bank of Baroda UAE and ICICI Bank UAE may consider Indian income for high-net-worth NRIs with strong banking relationships. For UAE residents: Only UAE salary considered. Alternative: Show global investment portfolio, fixed deposits, or use higher down payment (50-60%) to compensate for income location.

Q. What documents do Indians need to buy Dubai property?

Required documents: (1) Valid passport (6+ months), (2) UAE visa/Emirates ID (residents) or entry stamp (visitors), (3) Proof of funds (bank statements showing down payment source via LRS), (4) PAN card (for Indian remittances), (5) Form A2 (RBI foreign remittance), (6) Passport photos. If financing: add salary certificate, bank statements, employment letter. The developer guides the full process—Svarn Development specializes in Indian investor documentation.

Q. Is AED 750,000 property enough for a UAE investor visa?

Yes, AED 750,000+ property purchase makes you eligible for a 2-Year Investor Visa (renewable). Covers spouse, children, and one domestic helper. AED 2 Million+ investment qualifies for 10-Year Golden Visa (includes parents). Important: Property ownership doesn’t automatically grant a visa—a separate application required through GDRFA (General Directorate of Residency and Foreigners Affairs). Processing: 2-4 weeks. Cost: AED 3,000-5,000 for a family.

Q. How long does it take Indians to buy Dubai property?

Ready property: 4-6 weeks (mortgage approval 2-3 weeks, legal checks 1 week, registration 1 week). Off-plan: Immediate booking (1-2 days), then payment plan over construction (18-36 months). LRS transfer: 3-7 days for Indian bank processing. Cash buyers: 7-10 days for ready property. Most time-consuming: RBI compliance and mortgage approval. Svarn Development streamlines documentation for Indian buyers—typically close in 30-45 days.

Q. Should Indians buy off-plan or ready property in Dubai?

Off-plan advantages: 10-20% cheaper than ready, flexible payment plans (40-50% post-handover works with LRS limits), capital appreciation during construction. Ready advantages: Immediate rental income (7-8% yields), no construction risk, instant Golden Visa eligibility. For NRIs from India: Off-plan better—stagger payments across LRS annual limits, capture appreciation. For UAE residents: Either works—ready if need immediate income, off-plan for capital gains.