In Dubai, your credit score directly impacts your ability to secure a mortgage, the interest rate you receive, and the property types you can buy. A score above 700 generally qualifies buyers for better loan terms, while scores under 650 limit options. Improving your rating before applying for a mortgage can unlock stronger buying power and long-term investment returns.

Buying property in Dubai has never been more attractive — especially in 2025, with expanding communities like JVC, Business Bay, and Downtown. But one factor many buyers overlook is their credit score.

Your credit rating isn’t just a number. It determines how much financing you can secure, the interest rate on your mortgage, and ultimately, the kind of home you can afford. Whether you’re eyeing an off-plan apartment in Jumeirah Village Circle or a luxury villa, understanding the role of your credit score is essential.

This guide explains exactly how your credit score affects your property-buying journey in Dubai, what minimum scores are needed, and how to strengthen your profile for better investment opportunities.

What is a Credit Score in the UAE?

In Dubai, your credit score directly impacts your ability to secure a mortgage, the interest rate you receive, and the property types you can buy. A score above 700 generally qualifies buyers for better loan terms, while scores under 650 limit options. Improving your rating before applying for a mortgage can unlock stronger buying power and long-term investment returns.

Buying property in Dubai has never been more attractive — especially in 2025, with expanding communities like JVC, Business Bay, and Downtown. But one factor many buyers overlook is their credit score.

Your credit rating isn’t just a number. It determines how much financing you can secure, the interest rate on your mortgage, and ultimately, the kind of home you can afford. Whether you’re eyeing an off-plan apartment in Jumeirah Village Circle or a luxury villa, understanding the role of your credit score is essential.

This guide explains exactly how your credit score affects your property-buying journey in Dubai, what minimum scores are needed, and how to strengthen your profile for better investment opportunities.

What is a Credit Score in the UAE?

A credit score in the UAE is a three-digit number (300–900) issued by Al Etihad Credit Bureau (AECB). It reflects your financial history, including:

✅ Credit card payments

✅ Personal and auto loans

✅ Mortgage history

✅ Telecommunications and utility bills

✅ Loan defaults or late payments

A high score signals lower risk to lenders, while a low score suggests difficulty in repayment.

Why Does Your Credit Score Matter in Dubai Real Estate?

Banks in Dubai rely heavily on your credit score when approving mortgages. It influences:

✅ Mortgage Eligibility – Scores above 700 usually get faster approval.

✅ Loan Amount – Stronger scores unlock higher financing limits.

✅ Interest Rates – Lower risk = better rates, saving thousands over time.

✅ Developer Payment Plans – Some developers, like Svarn Development with Sereno Residences, offer buyer-friendly payment structures but still require strong financial credibility.

What is the Minimum Credit Score for a Mortgage in Dubai?

Most UAE banks require a minimum credit score of 650 to qualify for a home loan. However:

✅ 650–699: Eligible for mortgages, but with higher interest rates.

✅ 700–749: Good range; access to better mortgage products.

✅ 750+: Excellent — unlocks premium mortgage deals with low rates.

Can You Buy Property in Dubai With a Low Credit Score?

Yes, but with limitations:

✅ You may qualify only for lower loan amounts.

✅ Expect higher down payments (up to 30–40%).

✅ Interest rates will be less favorable.

✅ Developers may restrict access to post-handover payment plans.

In such cases, off-plan properties with flexible payment structures may be a more realistic entry point than ready homes.

How to Improve Your Credit Score Before Buying a Property

If your score isn’t where it needs to be, follow these steps before applying:

✅ Pay bills on time – Utilities and telecom bills affect AECB reports.

✅ Reduce credit card debt – Keep usage below 30% of your credit limit.

✅ Avoid multiple loan applications – Each rejection lowers your score.

✅ Maintain older credit accounts – Length of history strengthens your profile.

✅ Check your AECB report – Correct any errors before applying for a mortgage.

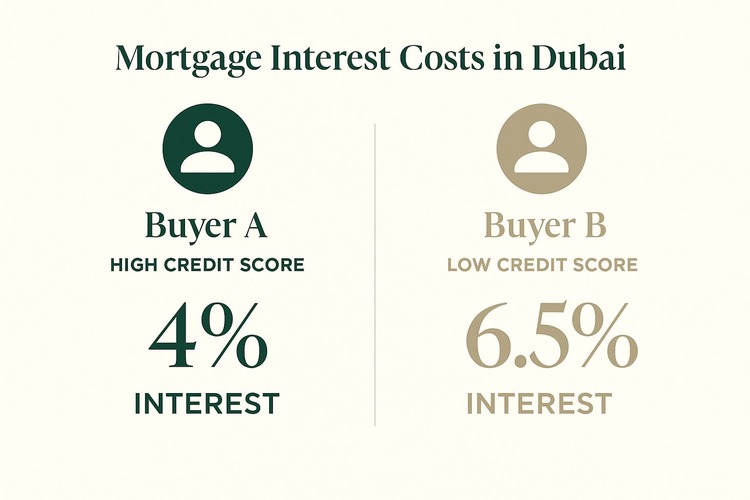

How Does Credit Score Affect Mortgage Interest Rates in Dubai?

Example:

✅ Buyer A: Credit Score 760 → Mortgage at 3.25% interest.

✅ Buyer B: Credit Score 650 → Mortgage at 4.5% interest.

Over a 25-year mortgage on AED 1M:

✅ Buyer A pays ~AED 458,000 in interest.

✅ Buyer B pays ~AED 635,000 in interest.

A difference of AED 177,000, just because of credit score.

Does Credit Score Affect Off-Plan Properties?

Yes — but differently. Developers offering off-plan projects like Sereno Residences by Svarn Development often provide 50-50 payment plans (50% during construction, 50% at handover).

While banks still review your credit profile for mortgage eligibility, off-plan purchases may give you more time to improve your score before the final mortgage payment stage.

Tips for First-Time Buyers in Dubai (2025)

✅ Check your credit score early (through AECB).

✅ Get pre-approved by a bank before property hunting.

✅ Target communities with strong ROI (JVC, Business Bay, Dubai Hills).

✅ Balance developer plans vs. bank mortgages depending on your credit rating.

Conclusion

In Dubai’s competitive property market, your credit score is the silent dealmaker. It shapes your mortgage approval, interest rate, and overall buying power. For investors and first-time buyers alike, taking steps to build and maintain a strong score ensures smoother financing and higher returns.

At Svarn Development, we believe every property journey should be transparent and future-proof. With projects like Sereno Residences, backed by flexible payment structures, you can turn your financial preparation into lasting property success.

Ready to explore? Discover more at Sereno Residences JVC.

FAQ’s

1. What is the minimum credit score needed to buy property in Dubai?

Most banks in Dubai require a minimum credit score of 650 to approve a mortgage. Scores between 700–749 unlock better loan terms, while a score of 750+ qualifies for the best interest rates and higher loan eligibility.

2. Can I get a mortgage in Dubai with a low credit score?

Yes, but it’s harder. With a score below 650, you may need to make a higher down payment (30–40%), accept higher interest rates, and qualify for smaller loan amounts. Some buyers opt for off-plan properties with flexible developer payment plans as an alternative.

3. How do banks in Dubai check my credit score?

Banks use the Al Etihad Credit Bureau (AECB) to access your credit history. The report includes loan repayments, credit card usage, telecom bills, and utility payments. Your score ranges from 300–900 and determines your mortgage eligibility.

4. Does my credit score affect mortgage interest rates in Dubai?

Yes. Buyers with higher scores receive lower mortgage interest rates, reducing long-term costs. For example, a buyer with a 760 score might get 3.25% interest, while a buyer at 650 may pay 4.5%, leading to a difference of over AED 175,000 in interest on a 25-year mortgage.

5. How can I improve my credit score before buying property in Dubai?

To raise your score:

✅ Pay all bills on time

✅ Keep credit card usage under 30%

✅ Avoid multiple loan applications

✅ Maintain older accounts for longer history

✅ Check your AECB report for errors

6. Does credit score matter for off-plan property in Dubai?

Yes, but less immediately. Developers like Svarn Development often offer 50-50 or post-handover payment plans. While you may not need full mortgage approval upfront, banks will still check your credit score when you finance the final handover amount.

7. Can foreigners buy property in Dubai with a low credit score?

Yes, but conditions apply. Expat buyers with lower scores may face stricter loan terms or need higher down payments. However, Dubai’s freehold areas allow expats to buy, and off-plan projects often provide more flexible payment structures.

8. Is 700 a good credit score in Dubai for buying property?

Yes. A credit score of 700+ is considered good in the UAE. It typically qualifies you for standard mortgage products with competitive interest rates and allows greater choice in property options.

9. What happens if my credit score drops after I get a mortgage in Dubai?

Once approved, your existing mortgage terms remain unchanged. However, a lower score may affect your ability to refinance or take new loans in the future. Maintaining good financial habits is key to long-term flexibility.

10. Do all developers in Dubai require credit score checks?

Not always. Developers selling off-plan units often rely on payment plan structures instead of immediate mortgage approval. However, if you require financing at handover, the bank will still assess your credit score.